Deciding between renting and buying is a significant choice that should not be taken lightly. While it may not be as simple as choosing between Apple or Samsung, where you choose to live has long-lasting effects and involves a considerable financial commitment.

The decision to buy or rent a house ultimately depends on your financial situation and personal goals. It is important to consider factors such as being debt-free, having a sufficient emergency fund and down payment, and ensuring that your mortgage payment does not exceed 25% of your take-home pay. We will delve into these aspects further.

If you are currently paying off debt or anticipate a job relocation, it may be wiser to opt for renting as it offers more flexibility. Contrary to popular belief, renting is not a waste of money. Housing is a necessary expense, unlike spending money on lottery tickets, which can be considered as throwing money away.

Choosing where you live wisely is one of the most effective ways to take control of your financial situation.

Is It Better to Rent or Buy?

The ongoing debate between renting and buying has gained significant attention in recent years due to the volatile housing market. It is important to keep in mind that the decision of whether to rent or buy ultimately depends on your circumstances and financial situation. Both options have their advantages and disadvantages.

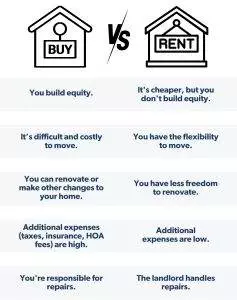

Purchasing a house provides the benefits of ownership, privacy, and the potential for building home equity. However, it is essential to consider the costs associated with expensive repairs, taxes, interest, and insurance.

On the other hand, renting a home or apartment requires lower maintenance and offers greater flexibility when it comes to relocating. Nevertheless, you may encounter challenges such as rent increases, noisy neighbors, or an uncooperative landlord.

Owning a home can undoubtedly be a source of pride and enjoyment, allowing you to bring your Pinterest-inspired home décor ideas to life. However, it is crucial to acknowledge that homeownership can also be a significant financial responsibility and a potential source of stress. Therefore, it is imperative to thoroughly evaluate your readiness to buy a house before taking this significant step.

Pros and Cons of Buying and Renting

The pros and cons discussed here do not alter the answer to the question of whether one should buy or rent. Instead, they serve to assist you in making the right decision for your situation. It is important to consider that even if you are financially prepared to buy a home, you might not be considering potential future repairs. Similarly, while you may be fond of a trendy apartment, it is possible that it could come with bothersome neighbors. Now, let’s explore the advantages and disadvantages of both buying and renting.

Buying Pros

Acquiring a house grants you the status of a homeowner. Unlike renting, where your money does not contribute towards building equity, paying off your mortgage gradually leads to complete ownership of your home. Ultimately, once your mortgage is fully paid, you can experience the satisfaction of successfully materializing the American dream.

The value of your home has the potential to appreciate over time, depending on market conditions and the level of maintenance. For example, a property bought for $300,000 today could potentially be sold for $360,000 in the future.

Homeownership brings along tax advantages. Certain costs associated with owning a home, such as property taxes and mortgage interest, can be deducted from your taxes.

As a homeowner, you have the freedom to make renovations to your house according to your preferences. You have the authority to make any desired changes without interference from a landlord. However, it is advisable to consider your spouse’s opinion, even when it comes to bold choices like painting your house in a hot pink color.

Owning a house offers increased privacy compared to living in an apartment. In an apartment, arguments between couples can be easily heard due to the thin drywall. However, owning your own house allows you to avoid such disruptions and enjoy a peaceful living environment. It is important to note that this advantage may not apply if you prefer a condo in a bustling city with bright lights.

Buying Cons

Traveling and relocating have become more complex in recent times. Whether you’re planning a spontaneous trip to Southeast Asia for 6 months or moving for work, there is now a greater need for preparation. This includes terminating your lease, packing your belongings, and purchasing a one-way ticket to an unfamiliar destination. The same applies to work-related relocations, where you’ll need to make arrangements to either rent out or sell your house, or ensure it remains vacant for an extended period.

It is important to be aware of the increased expenses involved when transitioning from renters insurance to homeowners insurance. Additionally, you should consider the potential costs associated with a flood policy, homeowners association (HOA) fees, property taxes, and higher utility bills. These factors collectively contribute to a rise in monthly expenses.

If you are a homeowner and find yourself dealing with a leaky roof, it can be a significant issue that may require dipping into your emergency savings to fix or replace the entire roof. However, if you are a tenant, managing a leaky roof is a simpler process. Just place a bucket under the leak and inform your landlord, and they will handle the necessary repairs.

When purchasing a home, it is important to save money for a down payment and closing costs. Buying a home requires dedication and effort, especially for those embarking on their first home-buying journey. It is advisable to save and contribute 5-10% of the property’s purchase price as a down payment.

Renting Pros

Renting provides the opportunity to easily change locations, allowing you to break free from the monotony of staying in one place. It also offers the advantage of simpler lease terminations compared to dealing with a mortgage. Another perk of renting is that maintenance is provided free of charge, eliminating the need to contact a plumber or visit an appliance store for repairs. Renters also enjoy the immediate cost-effectiveness of lower insurance premiums and move-in costs, as well as the absence of high HOA fees or private mortgage insurance (PMI) once settled in.

Renting Cons

Rent rates are expected to experience upward trends over time. This implies that even if you were successful in securing a favorable deal in a sought-after location, factors such as inflation, competition, and the appreciation of property values will result in annual rent increases. Unfortunately, there are no financial incentives available to offset this. Without any tax deductions, equity, or the potential for increasing property value, it is possible to feel financially stagnant despite allocating your rent money toward an essential living expense. Additionally, it is important to note that making renovations to the rental property is not within your freedom. While upgrading the bathroom with new tiles can greatly enhance its appearance, it is crucial to seek your landlord’s approval, as they are responsible for any renovations. Even minor alterations, such as selecting paint colors, may require permission.

Now you have all the information you need! Whether you’re prepared to make a purchase or prefer to continue renting, you now have a clearer understanding of what to expect.

Is it Always Cheaper to Rent?

When comparing the costs of renting and buying a property, it is generally found that renting an apartment is more affordable than buying a house. However, it is important to note that renting a house instead of an apartment may result in higher costs compared to the mortgage payment for the same house. The overall price can vary significantly depending on the location.

If we focus solely on monthly expenses, homeownership tends to lean towards the more expensive side due to additional costs such as maintenance, taxes, and homeowners insurance on top of the mortgage payment.

Renting an apartment may be a more cost-effective option, especially in markets where houses are excessively expensive, such as San Francisco.

Nevertheless, there is a tipping point to consider. If you continue renting for many years, you may end up paying more compared to if you had purchased a house initially. This is because mortgage payments remain stable while rents tend to increase (unless you have an adjustable-rate mortgage, which may also lead to an increase in your mortgage payment). Therefore, if you plan to stay in one place for a long time, it is generally better to buy a home, particularly when you eventually pay off your mortgage.

Should I Buy a Home Now?

To ensure a smooth home-buying process, it is crucial to have your financial affairs in order. This involves prioritizing debt repayment, establishing an emergency fund that covers 36 months of expenses, and then focusing on saving for a down payment.

For individuals purchasing their first home, I recommend aiming for a down payment of at least 5-10% on a 15-year fixed-rate mortgage. It is advisable to steer clear of FHA and VA loans. By saving 20% for a down payment, you can avoid the cost of private mortgage insurance (PMI), potentially saving a significant amount of money each month.

When determining your budget for a house, ensure that your mortgage payment, which includes principal, interest, property taxes, homeowners insurance, PMI, and HOA fees, does not exceed 25% of your take-home pay.

Factors to Take into Account When Determining Whether to Rent or Buy

When deciding to rent or buy, it is crucial to prioritize your financial situation. If you find yourself burdened with debt or lacking a down payment, it may not be feasible for you to purchase a house.

However, if your finances are in good shape, there are other factors to take into account. The location is a significant consideration. Renting may be more affordable if you desire to live in a city or area with high-performing schools and expensive homes. On the other hand, you could opt to buy a house in a different part of town where prices are more reasonable, but you may have to compromise on school or commute.

Another aspect to think about is your long-term plans. If you anticipate moving to a different city within a few years, it is advisable not to buy a home there. Typically, it is recommended to stay in a house for a minimum of three years to avoid financial losses when selling.

Additionally, once you become a homeowner, you must be willing and capable of maintaining the property. Tasks such as mowing the lawn, cleaning gutters, and replacing furnace filters will need attention, either by yourself or through hiring professionals (which incurs costs). There will always be something that requires fixing when owning a home.

While owning a home has its advantages, it is important to remember that repair and maintenance expenses can accumulate. Therefore, it is essential to consider more than just the monthly rent or mortgage payment.

Determining the Financial Implications of Renting vs. Buying a House

To make an informed decision about whether to rent or buy, it’s important to understand how to analyze the financial aspects of both options.

To determine the cost of renting, start by searching online for available rentals in the desired neighborhood. Rental listings should provide information on the monthly rent, as well as any additional fees such as utilities or parking charges. It’s crucial to take into account any potential hidden fees, such as elevator or garbage fees, that may be added by the apartment complex. Additionally, if you have a pet, be aware that there may be a pet fee involved.

To estimate the cost of buying a house, conduct an online search to get an idea of the prices of houses that meet your preferences and budget. You can then use a mortgage calculator to calculate your monthly payment, taking into consideration factors such as the purchase price, down payment, interest rate, property taxes, homeowners insurance, and HOA dues. It’s recommended that your monthly payment does not exceed 25% of your take-home pay. Additionally, budget around $300 a month for utilities, such as electricity, gas, water, and sewer, and allocate at least an additional $100 for internet, streaming services, and trash collection.

Let’s consider an example for a $300,000 home. Assuming a 15-year mortgage with a 6.25% interest rate and a 20% down payment, the total monthly payment, including taxes, insurance, and HOA dues, would be approximately $2,550. Adding the estimated $400 for utilities and other services, the total monthly cost would be around $3,000. If this number seems overwhelming, it may be necessary to explore more affordable housing options or continue renting.

3 Key Reasons to Avoid Buying a House

During my conversations with numerous home buyers, I often encounter individuals who express regret over their purchases due to making the wrong decision. You must avoid falling into the same predicament as them. Therefore, it is essential to consider the following reasons why purchasing a house may not be advantageous.

1. It’s a “great” deal.

Buying a house is a significant decision, especially when considering the financial aspects. While it may seem tempting to jump at a seemingly great deal, it is essential to approach real estate purchases with caution. Instead of solely focusing on market conditions, it is wiser to prioritize finding the right home at the right time. Rushing into a purchase without considering affordability could result in financial strain. It is advisable to exercise patience and remember that there will always be other opportunities for good deals in the future.

2. Feeling pressured?

Many individuals in their 20s and 30s often experience significant pressure to purchase a house as they believe it to be a sign of maturity. However, the reality is that taking control of your finances is the most mature step you can take.

Therefore, if you’re 25 and feel like you’re falling behind because you haven’t purchased a house yet, there’s no need to worry. It is important not to rush into such a significant investment simply because your friends or family are urging you to do so. Remember, you are unaware of their financial situation, and it is unwise to take advice from individuals who may not be financially stable.

Being an adult means recognizing that homeownership may not always be the best financial decision for everyone. It is far more sensible to wait until you are financially prepared before making such a commitment. Trust me when I say that nobody has ever regretted waiting until they were truly ready, especially when it comes to buying a house!

3. You have plans to relocate within the next few years.

If you are dissatisfied with your current living situation, it would not be wise to purchase a home in that area. Similarly, it would not be logical to buy a house if you are aware that you will be moving for work or family reasons within the next year or two. It is important to ensure that you are prepared to establish long-term stability before making a home purchase.

3 Times When You Should Rent

It is important to emphasize that renting is not a wasteful expenditure. Although you are giving your money to the landlord, you are receiving the benefit of having a place to live. Therefore, as long as you are paying for a living space, your money is being utilized wisely.

Although I do not advocate for renting as a long-term solution, there are certain situations where renting may be more advantageous than buying.

1. You are in the process of repaying your debts.

If you happen to have student loans, credit card bills, or any other debt to repay, think of your apartment as the perfect place to focus on this mission. By having affordable renters insurance and relying on your landlord to cover maintenance expenses, you can allocate more resources toward paying off your debts.

In case your rent is taking up a significant portion of your income, it might be worth considering a more affordable apartment. This will provide you with a greater chance to eliminate your debts and save money in the process.

2. Your employment requires you to move around.

If you are serving in the military or have short-term plans in an area, it is more advisable to opt for renting. Typically, it is necessary to reside in a property for a duration of two to three years to justify the initial expenses associated with purchasing a house.

3. It is essential to allocate sufficient time for creating a plan.

Purchasing a house involves a significant long-term commitment. Similar to any relationship, making impulsive decisions is not advisable. Therefore, if you have recently married, completed your college education, or are uncertain about the ideal neighborhood to reside in, it is wise to opt for renting for some time. I suggest waiting for at least a year as this will provide you with the opportunity to determine the proximity you desire to your in-laws.